Newest California Foreclosure Timeline

Newest California Foreclosure Timeline Graph

Sacramento Short Sale Specialist and Certified Foreclosure Options Specialist Forth Hoyt Answers The Most Common Questions About Foreclosure Time Lines In California-

How much time do I have in my home?

Am I in Foreclosure?

What is the foreclosure process time line?

How long till the bank forecloses?

How long does it take the bank to foreclose?

What is the foreclosure process and how much time does foreclosure take?

What is California’s newest foreclosure timeline?

I talk to people all day long who have the same questions… these have been a source of many of my posts here…

The answer is: it depends; nearly every homeowners experience is different…

I personally know people who were foreclosed on in less than eight months and others that have been living in their home for over three years without making a payment and haven’t hear a PEEP from the bank… Three years payment free and the foreclosure process has not even been started on their home!

The most important thing you can do, it you are worried about where you are in the process and you want to find out whether the bank has started foreclosure and how fast the foreclosure process is moving, is to align yourself with a real estate agent who is specializing in foreclosures, foreclosure options and helping homeowners understand their options…

This agent will have the tools and know-how to quickly research what is happening in your situation and give you options, explain the pitfalls and tell you what your best plan of action may be.

Are you considering doing a loan modification? Contact us today and we will forward you a new report:

Back to the Foreclosure time-lines:

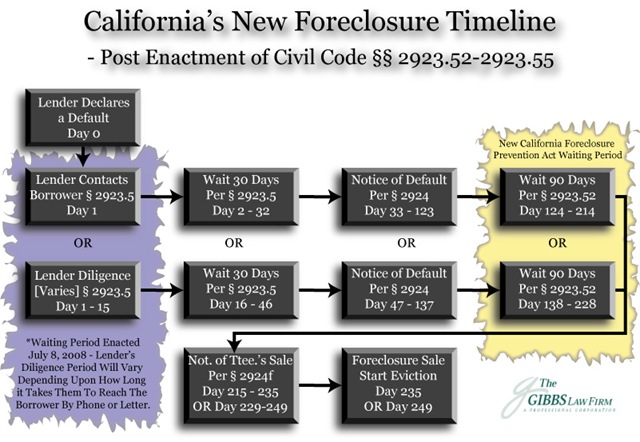

California passed a new foreclosure timeline law in 2008.

Here’s the entire report from the Association of Realtors:

California Association of Realtors

When a real estate transaction involves a property in foreclosure, knowing the foreclosure timeline helps you as the real estate agent to assess whether you have enough time to close escrow before the foreclosure sale. Starting September 8, 2008, California has a special foreclosure timeline for loans originated between 2003 and 2007, inclusive, which are secured by owner-occupied residences. Indeed, loans involved in short sales are likely to be owner-occupied loans from the years 2003 to 2007, which was the heyday for subprime lending. The special foreclosure timeline does not apply if the borrower has filed for bankruptcy, surrendered the property, or contracted with a person or entity whose primary business is advising people, who have decided to leave their homes, on how to extend the foreclosure process and avoid their contractual obligations. The special foreclosure timeline will remain in effect until January 1, 2013. (Cal. Civ. Code § 2923.5.)

FORECLOSURE TIMELINE FOR OWNER-OCCUPIED REAL PROPERTY LOANS (made from 2003 to 2007)

The approximate minimum time frames for the non-judicial foreclosure of owner occupied real property loans made from 2003 to 2007 are as set forth below. In California, most lenders elect to foreclose non-judicially by conducting trustees’ sales, not by judicial foreclosure.

Pre-Foreclosure Period

A lender may initiate the foreclosure process when a borrower defaults on a loan, such as by missing a mortgage payment. However, a slight delay may not justify acceleration and foreclosure by the lender. Hence, in practice, lenders generally wait a few months after a missed payment before starting the foreclosure process.

Day 1: Lender Contacts Borrower

For owner-occupied loans from 2003 to 2007, a lender initiating the foreclosure process must generally contact the borrower by phone or in person to assess the borrower’s financial situation and explore options for avoiding foreclosure. During the conversation, the lender must inform the borrower of the right to meet with the lender within 14 days. The lender must also give the borrower the toll-free number for finding a HUD-certified housing counseling agency.

Day 31: Filing of Notice of Default

For owner-occupied loans from 2003 to 2007, the lender may file a notice of default 30 days after contacting the borrower to explore options for avoiding foreclosure. The notice of default must be filed in the county where the property is located and a copy must be mailed within 10 business days after recordation to the borrower and all other persons who have requested such notice. The notice of default informs the borrower of the default. It must also include the lender’s declaration that it has contacted the borrower to explore options for avoiding foreclosure, tried with due diligence to contact the borrower, or the borrower has surrendered the property.

Day 121: Filing of Notice of Trustee’s Sale

Three months after the filing of the notice of default, the lender may record a notice of trustee’s sale setting forth the date, time, and place of the upcoming trustee’s sale. Because of the gravity of a notice of trustee’s sale, it must be widely disseminated. The notice of trustee’s sale must be recorded, posted, mailed to the borrower and others, as well as published once a week for three consecutive weeks in a newspaper of general circulation.

Day 145: Deadline to Cure Default

Up to five business days before the trustee’s sale, the borrower may reinstate the loan by curing the default or paying the missed payments plus allowable costs. After the reinstatement period expires, the borrower still has the right to redeem the property by paying the entire debt, plus interest and costs (not just the arrearage), before the bidding begins at the trustee’s sale.

Day 152: Trustee’s Sale

Although California law allows a trustee’s sale to take place 20 days after the posting of the notice of trustee’s sale, lenders customarily wait at least 31 days instead to help protect against federal tax liens. At the trustee’s sale, the property is sold through a public auction to the highest bidder. Title is transferred to the successful bidder by trustee’s deed.

USING THIS FORECLOSURE TIMELINE

A foreclosure timeline helps you as a listing agent ascertain whether you have enough time to market and sell the property as a short sale. Depending on the stage of foreclosure the homeowner is in (“Foreclosure Stage”), the chart below gives you the total time frame you have, at a minimum, to sell a property as a short sale before the trustee’s sale occurs (“Minimum Time Left to Sell”).

As an example, if a notice of default has just been filed, you have a minimum of about four months to sell the property before the trustee’s sale may occur. That’s four months not only to find a buyer, but also to get the lender to approve the short sale and close escrow. The short sale lender may agree to postpone the trustee’s sale in some situations (such as when there’s an accepted offer), but be sure to get any agreement for a postponement in writing.

FORECLOSURE TIMELINE FOR OTHER TYPES OF LOANS

For loans that are not secured by owner-occupied real property or not made from 2003 to 2007, lenders are not required to contact the borrowers to explore options for avoiding foreclosure. For these loans, the total minimum timefor the foreclosure process is roughly only 122 days, not 152 days. If the lender is not required to contact the borrower, the foreclosure process takes a minimum of about 4 months from the filing of the notice of default to the day of the trustee’s sale.

So why are you reading this?

More and more of the people I talk to who are trying to do a loan mod or are prospects for a short sale that I talk to are still current but have reached the end of their rope… many of them made substantial down payments and were counting of home equity for their retirement and are having a hard time facing the fact that they have to let their home go.

It seems that even those who have never lost a job, but their spouse has, maybe they have seen reduced over-time, or a failed home-based business or at least a business that is no longer producing as much income… or spouses that are no longer works part time… People are finding their credit cards maxed . And no longer have the ability to tap their home equity to periodically to pay down credit cards or upgrade automobiles…

By the way; what Government programs can you qualify for?

CHECK ELIGIBILITY NOW

Take action, find out more about your options and learn if you are eligible. If your situation is urgent, or you have further questions, feel free to Contact us Today At Forth Hoyt’s Sacramento Short Sale Center

{kind=link}

{kind=link}